What Is Business Insurance? – A Complete Beginner’s Guide

Introductory Hook

Imagine launching your dream venture… the late-night brainstorming, the excitement, the hope. But then—unexpectedness strikes: a customer slips, data vanishes, or a fire damages your workspace. Suddenly, that dream teeters on collapse.

This is where business insurance steps in. I’ve been there—navigating uncertainty, seeking safety nets. In this guide, I’ll walk you through everything you need to know to protect your business, with clarity and heart.

Table of Contents

- What Is Business Insurance?

- Why It Matters

- Common Types of Business Insurance

- General Liability

- Property Insurance & Business Interruption

- Business Owner’s Policy (BOP)

- Workers’ Compensation & Commercial Auto

- Professional Liability (E&O)

- Cyber Insurance

- Key Person Insurance

- Step-by-Step: How to Get Business Insurance

- Cost Factors & Typical Premiums

- How to Choose the Right Coverage

- Hostinger Hosting Offer

- Key Takeaways

- FAQs

- Conclusion

- Sources

1. What Is Business Insurance?

Business insurance is like a safety glove for entrepreneurs. It’s a set of policies designed to shield your venture from financial hits due to events like lawsuits, accidents, or disasters. It keeps your business resilient when the unexpected happens. (Link-Hellmuth Insurance, Lloyds Bank)

2. Why It Matters

Some incidents can seem small—yet devastate your future:

- Customer sues for slip-and-fall.

- Server crash erases client data.

- Fire shuts operations for weeks.

Business insurance helps you bounce back, avoiding catastrophic financial loss—or worse, business closure. (Small Business Administration, Investopedia)

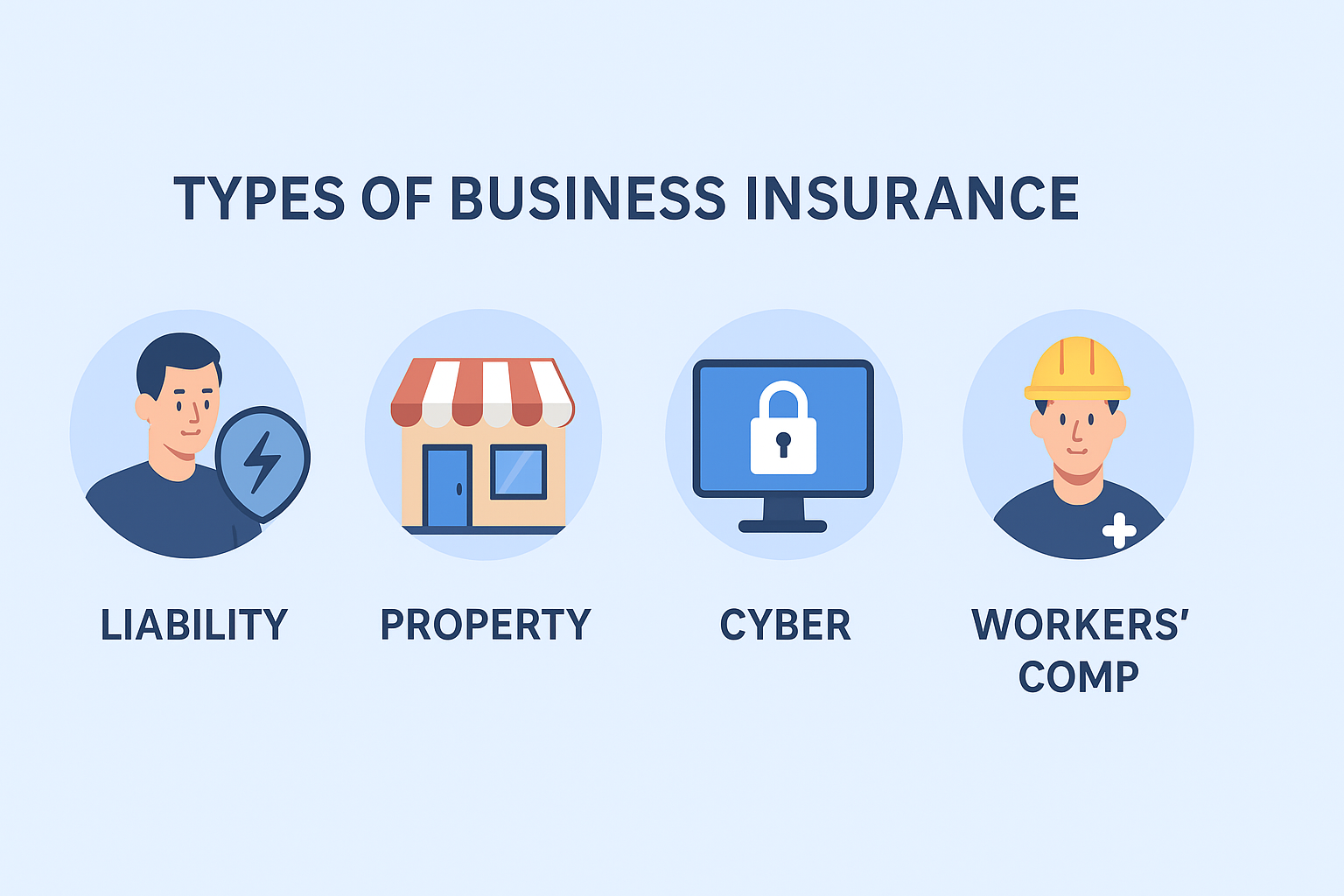

3. Common Types of Business Insurance

General Liability Insurance

Covers claims like bodily injury, property damage, or advertising injury. Often the first policy small businesses purchase. (NerdWallet, Insurance Business America)

Property Insurance & Business Interruption

Protects physical assets—equipment, inventory, premises. Business interruption insurance covers lost income when operations halt after a covered disaster. (sentry.com, Wikipedia)

Business Owner’s Policy (BOP)

A smart bundle combining general liability and property insurance—usually cheaper than buying separately. (Wikipedia)

Workers’ Compensation & Commercial Auto Insurance

Often legally required. Workers’ comp covers employee injuries; commercial auto covers business vehicle operations. (Small Business Administration, Insureon)

Professional Liability Insurance (Errors & Omissions)

Necessary for service providers. Covers legal costs when clients claim negligence or unsatisfactory service. (Wikipedia)

Cyber Insurance

Protects against digital threats like data breaches, ransomware, and cyberattacks. Covers restoration, legal fees, and lost income. (Insurance Business America)

Key Person Insurance

Insures the loss of a key individual (like a founder or critical employee) — helps recover business continuity and profits. (Wikipedia)

4. Step-by-Step: How to Get Business Insurance

- Evaluate Risks – List what could derail your business: injuries, cyber threats, property damage. (Insureon, Investopedia)

- Research Coverage Types – Match risks to insurance types.

- Compare Quotes – Get at least three quotes; consider bundling via a BOP for savings. (Investopedia, Insureon)

- Buy Policy – Review coverage, limits, deductibles with a broker if needed.

5. Cost Factors & Typical Premiums

Costs vary by factors like business type, location, coverage limits, and claims history. Here’s a snapshot of typical U.S. monthly premium ranges:

| Insurance Type | Monthly Cost (USD) |

|---|---|

| General Liability | $25 – $115 (Wall Street Journal) |

| Commercial Auto | $125 – $575 (Wall Street Journal) |

| Workers’ Comp | $35 – $120 (Wall Street Journal) |

| Cyber Insurance | $40 – $145 (Wall Street Journal) |

| BOP (Annual) | ~$300+ (Investopedia) |

Saving tips: bundle policies, raise deductibles, shop annually, consult brokers. (Wall Street Journal, Investopedia)

6. How to Choose the Right Coverage

- Know what your state mandates (e.g., workers’ comp, auto).

- Assess real risks based on your business nature, size, and assets.

- Consider bundling with BOP for cost-efficiency.

- Review policy terms to avoid coverage gaps. (Investopedia)

7. Key Takeaways

- Business insurance is essential protection against financial setbacks.

- Key types include liability, property, BOP, workers’ comp, professional, cyber, and key person coverage.

- Evaluate risks, compare quotes, and consider bundling to save.

- Premiums vary—know what you need and shop smart.

- Use Hostinger to build your online presence affordably with a 20% discount.

8. Frequently Asked Questions (FAQ)

Q: Is business insurance mandatory?

A: Some types are required by law (e.g., workers’ comp, commercial auto). Others like general liability are highly recommended.

Q: Can I bundle policies?

A: Yes — BOP bundles general liability and property, often lowering cost.

Q: What is business interruption insurance?

A: It covers lost income when your business can’t operate due to a covered disaster.

Q: Do home-based businesses need insurance?

A: Yes—you may need added coverage or riders, depending on assets and risk.

9. Conclusion

Building a business is fulfilling—and a bit nerve-racking. But with the right insurance, you can weather storms and keep moving forward. From covering basic liability to insuring your linchpin employees or digital risks, planning ahead is smart.

Write with confidence. Protect what you build. You’ve got this.